Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

At Infinity Market Research, we do not just deliver data - we deliver clarity, confidence, and competitive edge.

In a world driven by insights, we help businesses unlock the infinite potential of informed decisions.

Here is why global brands, startups, and decision-makers choose us:

Industry-Centric Expertise

With deep domain knowledge across sectors - from healthcare and technology to manufacturing and consumer goods - our team delivers insights that matter.

Custom Research, Not Cookie-Cutter Reports

Every business is unique, and so are its challenges. Thats why we tailor our research to your specific goals, offering solutions that are actionable, relevant, and reliable.

Data You Can Trust

Our research methodology is rigorous, transparent, and validated at every step. We believe in delivering not just numbers, but numbers that drive real impact.

Client-Centric Approach

Your success is our priority. From first contact to final delivery, our team is responsive, collaborative, and committed to your goals - because you are more than a client; you are a partner.

Recent Reports

Obesity Management Market

GLP-1 Receptor Agonist Market

Direct Air Capture Market

Direct Air Capture Market (By Source (Electricity, Heat, Other Source), By Technology (Solid-DAC, Liquid-DAC, Electrochemical-DAC, Other Technology), By Application (Carbon Capture, and Storage (CCS), Carbon Capture Utilization and Storage (CCUS), Other Applications), By End-Use Industry (Oil & Gas, Food and beverage, Automotive, Chemicals, Healthcare, Others End-Use), By Region and Companies)

Jul 2024

Energy and Power

Pages: 138

ID: IMR1182

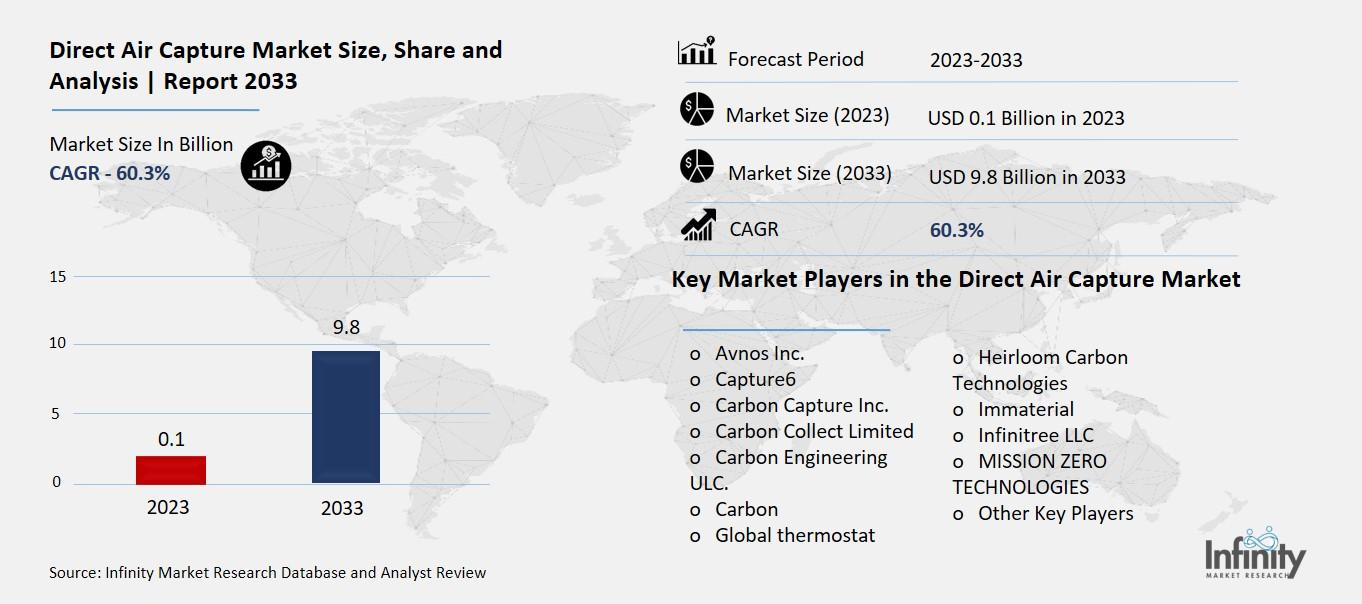

Direct Air Capture Market Overview

Global Direct Air Capture Market size is expected to be worth around USD 9.8 Billion by 2033 from USD 0.1 Billion in 2023, growing at a CAGR of 60.3% during the forecast period from 2023 to 2033.

The Direct Air Capture (DAC) Market is about companies and technologies that are working to remove carbon dioxide (CO2) directly from the air. CO2 is a greenhouse gas that contributes to climate change, so taking it out of the atmosphere can help reduce global warming. DAC technology uses machines to pull in air, capture the CO2, and then either store it safely underground or use it to make products like fuels or building materials.

This market is growing because people and governments are becoming more aware of the need to fight climate change. Investing in DAC technology can be part of the solution to reduce the amount of CO2 in the air. While it's still a new and developing field, more companies are getting involved, and more money is being put into research to make the technology better and cheaper. This is important because the more we can scale up DAC, the bigger the impact it can have on reducing the effects of climate change.

Drivers for the Direct Air Capture Market

Government Policies and Regulations

One of the primary drivers is the increasing implementation of government policies and regulations aimed at reducing greenhouse gas emissions. Countries worldwide are setting ambitious targets for carbon neutrality, and direct air capture technology is seen as a crucial tool in achieving these goals. Governments provide incentives, subsidies, and support for DAC projects to encourage adoption and innovation in this space. For instance, the United States and European Union have been particularly proactive, with policies that support carbon capture initiatives and integrate them into broader environmental strategies.

Technological Advancements

Advancements in DAC technology have significantly enhanced its efficiency and reduced costs, making it a more viable solution for large-scale deployment. Innovations in materials and processes have improved the capture rates of CO2 from the atmosphere, and ongoing research and development are expected to drive further improvements. As the technology matures, the cost per ton of CO2 captured is projected to decrease, making it more accessible for a wide range of applications. This technological progress is crucial for the scalability and economic feasibility of DAC systems.

Corporate Sustainability Goals

Corporate commitments to sustainability and carbon neutrality are another significant driver. Many companies, especially those with high emissions, are integrating DAC into their strategies to offset hard-to-abate emissions. Businesses are increasingly recognizing the importance of reducing their carbon footprint to comply with regulations and meet consumer demand for environmentally responsible practices. By investing in DAC technologies, companies can enhance their sustainability profiles and align with global efforts to combat climate change.

Public and Private Investment

There is a growing influx of investment from both public and private sectors into DAC projects. Governments are funding research and infrastructure development, while private investors see potential in the market's growth prospects. Major corporations are also investing in DAC technology as part of their environmental, social, and governance (ESG) strategies. This financial support is essential for scaling up operations and developing the necessary infrastructure to capture and store CO2 on a large scale.

Climate Change Awareness

Increasing awareness of the impacts of climate change among the public and stakeholders is driving demand for effective carbon removal solutions. As the effects of climate change become more apparent, there is a heightened sense of urgency to adopt technologies that can mitigate these impacts. Direct air capture is seen as a promising approach to removing existing CO2 from the atmosphere, complementing efforts to reduce emissions at the source.

Restraints for the Direct Air Capture Market

High Costs of Technology

The Direct Air Capture (DAC) market faces significant restraints, primarily due to the high costs associated with the technology. DAC systems require advanced machinery and materials to capture CO2 directly from the atmosphere, which can be very expensive. The initial capital expenditure for setting up these systems, along with the operational costs, is a major hurdle. This makes DAC less economically viable compared to other carbon capture and storage (CCS) methods, especially in its current nascent stage. The technology is still evolving, and substantial investment is needed to make it more cost-effective.

Energy-Intensive Process

Another major restraint is the energy intensity of DAC systems. Capturing CO2 from the air requires a lot of energy, which can offset some of the environmental benefits if the energy comes from non-renewable sources. The process involves running fans to move large volumes of air through chemical solutions or sorbents, which consume a significant amount of electricity. This high energy requirement not only increases operational costs but also raises questions about the overall carbon footprint of the technology unless it is powered by renewable energy sources.

Limited Infrastructure

The lack of existing infrastructure for DAC is another challenge. There are currently very few DAC facilities worldwide, and building new ones requires extensive planning, resources, and regulatory approval. This limited infrastructure hampers the scalability of DAC technologies. Moreover, the captured CO2 needs to be transported to storage sites, which adds another layer of logistical and infrastructural complexity. Developing a comprehensive infrastructure network for DAC will take time and significant investment.

Regulatory and Policy Barriers

Regulatory and policy barriers also impede the growth of the DAC market. While some regions have supportive policies for carbon capture and storage, others lack clear regulations or incentives for DAC. This inconsistent regulatory environment creates uncertainty for investors and companies looking to develop and deploy DAC technologies. Stronger and more uniform policy support is needed to encourage the widespread adoption of DAC and to make it a viable solution for large-scale carbon removal.

Technical Challenges and Efficiency

The technical challenges associated with DAC are significant. The technology is still in its early stages, and many systems are not yet efficient enough to capture CO2 at a large scale. Current DAC methods need improvements in terms of capturing efficiency, reducing energy consumption, and minimizing operational costs. Additionally, developing scalable and modular DAC systems that can be deployed across various industries and geographies remains a critical technical challenge that needs to be addressed.

Opportunity in the Direct Air Capture Market

Growing Climate Change Mitigation Focus

The global emphasis on combating climate change creates a significant opportunity for the Direct Air Capture (DAC) market. As awareness of the detrimental effects of greenhouse gas emissions increases, governments and businesses are prioritizing carbon reduction initiatives. DAC technologies offer a promising solution by directly removing CO2 from the air, helping industries achieve carbon neutrality. This technology is crucial in global efforts to limit global warming, making DAC an essential tool for ensuring a sustainable future.

Economic Opportunities Through Carbon Utilization

One of the major opportunities in the DAC market is the potential for carbon utilization and monetization. Captured CO2 can be used in producing synthetic fuels, chemicals, and building materials. These carbon-negative products not only help offset emissions in other sectors but also open new revenue streams. By transforming captured CO2 into valuable commodities, industries can turn an environmental liability into a profitable asset, driving both innovation and economic growth.

Favorable Market Environment from Carbon Pricing Mechanisms

The implementation of carbon pricing mechanisms and regulatory incentives is another significant opportunity for the DAC market. Governments worldwide are introducing policies that put a price on carbon emissions, encouraging businesses to find cost-effective ways to reduce their carbon footprint. DAC technologies provide a viable solution for companies to comply with these regulations, enhancing their market competitiveness and promoting environmental responsibility.

International Collaboration and Knowledge Sharing

The DAC market benefits from the potential for international collaboration. Addressing climate change is a global challenge that requires coordinated efforts and cooperation among countries and industries. By sharing knowledge and fostering partnerships, stakeholders can accelerate the development and deployment of DAC technologies, reduce costs, and scale up efforts more effectively. Such collaborations can drive market growth and facilitate a global transition to a low-carbon economy.

Innovation and Technological Advancements

Continuous innovation and technological advancements present substantial opportunities in the DAC market. As research and development efforts progress, new and more efficient DAC technologies are emerging. These advancements improve the scalability and cost-effectiveness of DAC systems, making them more accessible to a broader range of industries and regions. Continued investment in R&D is crucial for driving technological breakthroughs that can enhance the feasibility and impact of DAC solutions.

Supportive Public and Private Sector Investments

Increased public and private sector investments are driving growth in the DAC market. Governments are offering grants and incentives to support the development of DAC technologies, while private investors are recognizing the potential for substantial returns. These investments are crucial for scaling up DAC projects, reducing costs, and making carbon capture technologies more widely available. The financial backing from both sectors underscores the growing recognition of DAC's role in achieving climate goals and promoting sustainability.

Trends for the Direct Air Capture Market

Emphasis on Carbon Neutrality

One of the major trends is the growing emphasis on carbon neutrality. Governments, businesses, and organizations worldwide are focusing on reducing their carbon footprint. DAC technologies play a crucial role in this effort by capturing CO2 directly from the atmosphere, helping industries offset their emissions and achieve carbon neutrality. This trend is crucial as it supports global initiatives to limit global warming and protect the environment for future generations.

Integration with Renewable Energy

Another key trend is the integration of DAC technologies with renewable energy sources. As the world shifts towards clean energy, there is a notable synergy between DAC and renewable technologies like solar and wind power. This integration not only reduces the carbon footprint of DAC operations but also enhances the environmental sustainability of these processes. By coupling DAC with renewable energy, industries can minimize their environmental impact while contributing to the broader goal of decarbonizing the energy sector.

Increase in Carbon Offsetting Initiatives

The rise of carbon offsetting and removal initiatives is also driving the DAC market. With the implementation of carbon pricing mechanisms and regulatory frameworks, industries are seeking cost-effective ways to offset their carbon emissions. DAC provides a viable solution for companies aiming to comply with these regulations and demonstrate their commitment to environmental responsibility. This trend is creating new opportunities for DAC technologies to be deployed and utilized more widely.

Advancements in Technology and Efficiency

Technological advancements and improvements in efficiency are significantly impacting the DAC market. Innovations in materials and processes are making DAC technologies more cost-effective and efficient. For instance, developments in sorbents and catalysts used in DAC processes are enhancing the capture and storage capabilities of these technologies. As DAC becomes more efficient, it becomes a more attractive option for industries looking to reduce their carbon emissions.

Government and Policy Support

Support from governments and policymakers is another important trend. Many governments are implementing policies and incentives to promote the adoption of DAC technologies. These include subsidies, tax credits, and grants for research and development. Such support is crucial for accelerating the deployment of DAC technologies and making them a viable solution for large-scale carbon capture.

Growing Investment and Partnerships

Lastly, there is a growing trend of increased investment and strategic partnerships in the DAC market. Companies and investors are recognizing the potential of DAC technologies and are investing heavily in their development and deployment. Strategic partnerships between technology providers and industrial players are also emerging, aimed at scaling up DAC operations and expanding their reach. This trend is driving market growth and fostering innovation in the DAC sector.

Segments Covered in the Report

By Source

o Electricity

o Heat

o Other Source

By Technology

o Solid-DAC

o Liquid-DAC

o Electrochemical-DAC

o Other Technology

By Application

o Carbon Capture, and Storage (CCS)

o Carbon Capture Utilization and Storage (CCUS)

o Other Applications

By End-Use Industry

o Oil & Gas

o Food and beverage

o Automotive

o Chemicals

o Healthcare

o Others End-Use

Segment Analysis

By Source Analysis

With a market share of about 77.2% in the Direct Air Capture market in 2023, electricity commanded a commanding position. The widespread availability and simplicity of DAC system integration with electric power sources account for this segment's predominance. Electricity is a vital resource for the process because it is essential for running the many DAC technologies' parts, like fans, pumps, and capturing systems.

Efforts to decarbonize the power sector are also reflected in the high percentage of DAC systems powered by electricity. The increasing ubiquity of renewable energy sources reduces the environmental impact of electrically driven direct air capture (DAC) systems, hence increasing their attractiveness to stakeholders seeking more environmentally friendly carbon capture options.

Although it makes up a lower share of the market, heat is a source for direct air capture that has the potential to increase the effectiveness and affordability of carbon capture procedures. By offering a cheap thermal energy source for the sorbent regeneration process, the use of geothermal energy or industrial waste heat can drastically lower the operating expenses related to DAC.

While heat-based direct air conversion (DAC) is still less common than electricity-based DAC, its popularity is rising. This is especially because it offers a viable approach to scaling up DAC technology by reducing energy inputs and utilizing industry and geothermal resource synergies. Heat as a source for DAC is anticipated to gain traction as developments continue and integration tactics change, providing a supplemental method of lowering the carbon footprint of the capture process.

By Technology Analysis

Solid-DAC (S-DAC), with a market share of about 44.8%, commanded a commanding position in 2023. The effectiveness of this segment in absorbing CO2 through solid sorbents materials that can absorb or adsorb carbon dioxide is what gives it its notoriety.

Durability, low energy consumption, and the possibility of sorbent regeneration are the main advantages of S-DAC technologies. Rapid improvements in this technique have resulted in lower operating costs and greater industry acceptance of sustainable carbon management strategies.

In contrast, a sizeable chunk of the market was accounted for by Liquid-DAC (L-DAC). This method collects carbon dioxide from the atmosphere using liquid solvents. Because of its scalability and deployment flexibility, it might be a good choice for a wide range of applications.

L-DAC continues to draw investment because of its potential for effectively processing huge volumes of air and its flexibility to existing infrastructure, especially in industrial settings, even though it has a smaller market share than S-DAC.

In the DAC market, electrochemical-DAC (E-DAC) is the new frontier. Despite having a smaller market share, its innovation in carbon capture is driving its growth. E-DAC directly transforms CO2 from the atmosphere into usable goods including chemicals, synthetic fuels, and even carbon-neutral materials using electrochemical processes.

Because of its low energy usage and the special chance it presents for the direct conversion of CO2 into products with a high market value, this industry is growing. As this field's research and development continue to progress, E-DAC is anticipated.

By Application Analysis

With a market share of over 60.2% in 2023, Carbon Capture and Storage (CCS) commanded a commanding position in the industry. Because it captures carbon dioxide and stores it underground in geological formations, this section is the leader in reducing CO2 emissions. The fact that CCS can greatly reduce the contribution of industrial emissions to climate change highlights its importance.

Its significant market share indicates that large-scale carbon removal technologies are widely acknowledged as being necessary to meet global climate targets. Government laws and incentives geared at lowering carbon footprints have strengthened CCS technology, making it a preferred option for businesses looking to adhere to environmental standards.

In the meantime, a significant player in the direct air capture sector is emerging: Carbon Capture, Utilization, and Storage (CCUS). Despite having a lower percentage than CCS, its significance is increasing. In addition to capturing and storing CO2, CCUS also uses it for other purposes, such as manufacturing chemicals, construction materials, and synthetic fuels.

By End-Use Analysis

Industry Oil & Gas captured almost 44.8% of the market in 2023, securing a commanding lead. This industry's desire to reduce carbon emissions from extraction, processing, and transportation led to its reliance on DAC technology. Oil and gas firms now have a practical way to reduce their environmental effect without sacrificing operational effectiveness because of DAC solutions.

With a sizeable chunk of the remaining market share, the food and beverage sector emerged as a prominent participant in the DAC market. Businesses in this industry use DAC technology to lower their carbon footprint at every stage of the supply chain, from manufacturing and processing to distribution and packaging. The food and beverage industry's use of DAC continued to rise with customer demand for sustainable products.

Because of the industry's dedication to sustainability and pressure from regulations to cut emissions, the automotive sector also witnessed a considerable adoption of DAC technology. Automakers addressed issues with air pollution and climate change by incorporating DAC solutions into their manufacturing processes to offset the carbon footprint of vehicle manufacturing.

The Chemicals and Healthcare sectors, which are inherently dependent on carbon-intensive materials and processes, also demonstrated encouraging increases in the implementation of DAC. Utilizing DAC technology, these industries reduced their environmental footprint and complied with ever-tougher rules and sustainability programs.

Regional Analysis

With a commanding 46.8% market share in 2023, North America was the clear leader in the Direct Air Capture (DAC) industry. The region's strong industrial infrastructure, technological developments, strict regulatory frameworks, and the rising need for carbon capture solutions across a range of industries are all considered contributing causes to this supremacy.

North America, led by the United States, is home to a wide range of industries, many of which rely significantly on DAC technology. The need for carbon capture technologies is being driven by sectors including industry, energy generation, and transportation to reduce greenhouse gas emissions and adhere to environmental standards.

To address environmental concerns and accomplish sustainability goals, the region's rapidly expanding population and increasing industrial activity are driving the demand for novel carbon capture systems. Consequently, the Asia-Pacific market is rising at a faster rate than other regions, which is indicative of the region's increasing significance in the global DAC market landscape.

Competitive Analysis

Prominent industry participants are making significant R&D investments to broaden their product offerings, thereby contributing to the further expansion of the direct air capture market. To increase their worldwide presence, market players are also engaging in a range of strategic initiatives. Notable changes in the industry include the introduction of new products, contracts, mergers and acquisitions, increased investment, and cooperation with other businesses. The direct air capture sector needs to provide affordable products to grow and thrive in an increasingly competitive and developing market environment.

Recent Developments

In 2023: Although DAC was still in its infancy, it was gaining traction, with multiple businesses striving to create and market various DAC technologies. Among the pioneers in this industry were some of the important players you listed, like Carbon Engineering, Climeworks, Global Thermostat, and Carbon.

In 2023: Climeworks worked with Great Carbon Valley, a creative project development and systems integrator based in Kenya, to explore the possibility of undertaking large-scale projects. Market Research Future, Inc. reports on the direct air capture market (21897).

Key Market Players in the Direct Air Capture Market

o Avnos Inc.

o Capture6

o Carbon

o Global thermostat

o Heirloom Carbon Technologies

o Immaterial

o Infinitree LLC

o MISSION ZERO TECHNOLOGIES

o Other Key Players

|

Report Features |

Description |

|

Market Size 2023 |

USD 0.1 Billion |

|

Market Size 2033 |

USD 9.8 Billion |

|

Compound Annual Growth Rate (CAGR) |

60.3% (2023-2033) |

|

Base Year |

2023 |

|

Market Forecast Period |

2024-2033 |

|

Historical Data |

2019-2022 |

|

Market Forecast Units |

Value (USD Billion) |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

By Source, Technology, Application, End-Use, and Region |

|

Geographies Covered |

North America, Europe, Asia Pacific, and the Rest of the World |

|

Countries Covered |

The U.S., Canada, Germany, France, U.K, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil |

|

Key Companies Profiled |

Avnos Inc., Capture6, Carbon Capture Inc., Carbon Collect Limited, Carbon Engineering ULC., Carbyon, Global thermostat, Heirloom Carbon Technologies, Immaterial, Infinitree LLC, MISSION ZERO TECHNOLOGIES, Other Key Players |

|

Key Market Opportunities |

International Collaboration and Knowledge Sharing |

|

Key Market Dynamics |

Government Policies and Regulations |

Frequently Asked Questions

1. What would be the forecast period in the Direct Air Capture Market?

Answer: The forecast period in the Direct Air Capture Market report is 2024-2033.

2. How much is the Direct Air Capture Market in 2023?

Answer: The Direct Air Capture Market size was valued at USD 0.1 Billion in 2023.

3. Who are the key players in the Direct Air Capture Market?

Answer: Avnos Inc., Capture6, Carbon Capture Inc., Carbon Collect Limited, Carbon Engineering ULC., Carbyon, Global thermostat, Heirloom Carbon Technologies, Immaterial, Infinitree LLC, MISSION ZERO TECHNOLOGIES, Other Key Players

4. What is the growth rate of the Direct Air Capture Market?

Answer: Direct Air Capture Market is growing at a CAGR of 60.3% during the forecast period, from 2023 to 2033.

Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

- Accurate & Verified Data:Our insights are trusted by global brands and Fortune 500 companies.

- Complete Transparency:No hidden fees, locked content, or misleading claims - ever.

- 24/7 Analyst Support:Our expert team is always available to help you make smarter decisions.

- Instant Savings:Enjoy a flat $1000 OFF on every report.

- Fast & Reliable Delivery:Get your report delivered within 5 working days, guaranteed.

- Tailored Insights:Customized research that fits your industry and specific goals.

Need custom data?

Get tailored segments, regions, competitors, or analyst support for this report.