Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

At Infinity Market Research, we do not just deliver data - we deliver clarity, confidence, and competitive edge.

In a world driven by insights, we help businesses unlock the infinite potential of informed decisions.

Here is why global brands, startups, and decision-makers choose us:

Industry-Centric Expertise

With deep domain knowledge across sectors - from healthcare and technology to manufacturing and consumer goods - our team delivers insights that matter.

Custom Research, Not Cookie-Cutter Reports

Every business is unique, and so are its challenges. Thats why we tailor our research to your specific goals, offering solutions that are actionable, relevant, and reliable.

Data You Can Trust

Our research methodology is rigorous, transparent, and validated at every step. We believe in delivering not just numbers, but numbers that drive real impact.

Client-Centric Approach

Your success is our priority. From first contact to final delivery, our team is responsive, collaborative, and committed to your goals - because you are more than a client; you are a partner.

Recent Reports

Obesity Management Market

GLP-1 Receptor Agonist Market

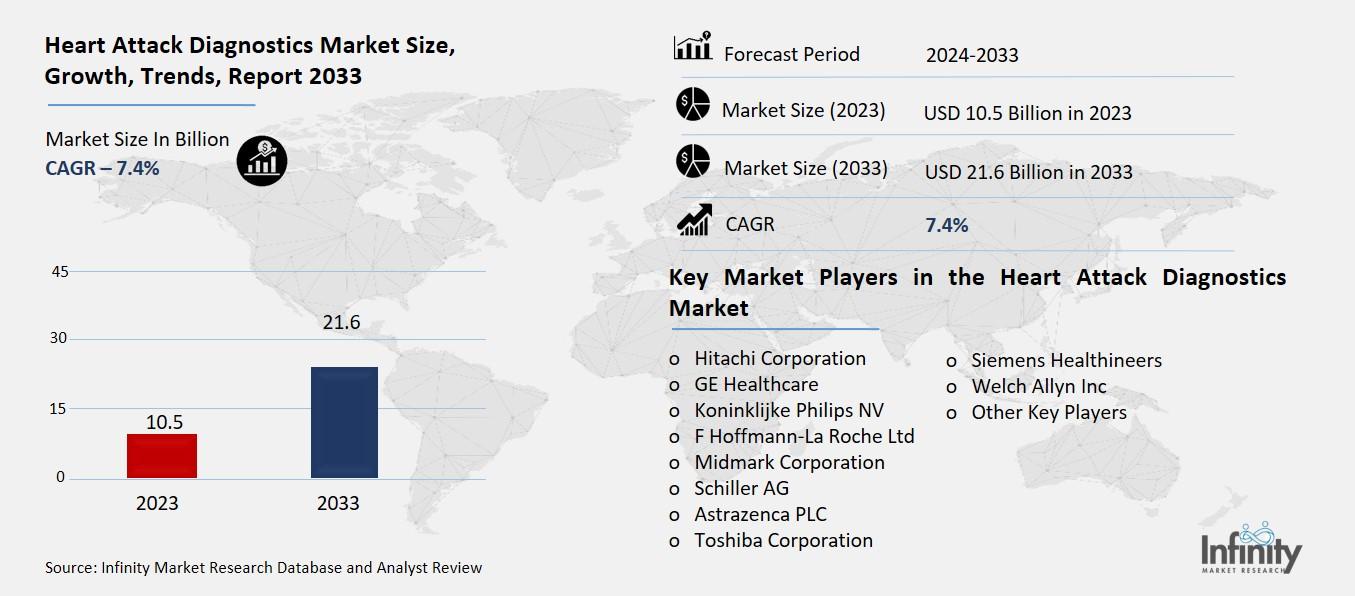

Heart Attack Diagnostics Market

Global Heart Attack Diagnostics Market (By Test, Computerized Cardiac Tomography, Electrocardiogram, Angiogram, Blood Tests, and Other Tests; By End-User Vertical, Hospitals, Diagnostic Centers, Ambulatory Surgical Centers, and Other End-User Verticals; By Region and Companies), 2024-2033

Jan 2025

Healthcare

Pages: 138

ID: IMR1408

Heart Attack Diagnostics Market Overview

Global Heart Attack Diagnostics Market acquired the significant revenue of 10.5 Billion in 2023 and expected to be worth around USD 21.6 Billion by 2033 with the CAGR of 7.4% during the forecast period of 2024 to 2033. The heart attack diagnostics market is a promising niche on the international level that is growing steadily due to the growth of cardiovascular diseases, the development of diagnostic tools, and the orientation to early detection. Diagnostic tests involve the use of an electrocardiology test, cardiac blood test for biomarkers like troponin, an echocardiographic test, and a computer tomography test. Given aspects like aging populations, modifiable health behaviors and increasing obesity levels rise the need for accurate and faster diagnostic tests. Next, advancement in technology such as POC testing, AI, and diagnostics methodologies are revolutionizing the market, and thereby enhancing precision and product availability.

Drivers for the Heart Attack Diagnostics Market

Rising Prevalence of Cardiovascular Diseases

The cause of increasing rates of heart attacks worldwide is several-fold concerning shifts in lifestyle, feeding patterns and even population demographics. Couch culture or lifestyles that require people to spend long hours seated, little chance of exercising and depending on gadgets affect their heart health. This sedentary nature culminates in factors that lead to susceptibility to a heart attack including, obesity, hypertensive, and type 2 diabetes. Eternalizing various risk factors associated with high cholesterol levels and narrowing arteries, poor diet as defined by the over- consumption of processed foods, high sugar and salt content diets, and low fresh fruit and vegetable intake contribute to the mentioned health risks. Furthermore, the global demographic factors are also at work here, as elderly persons are more likely to suffer from cardio vascular diseases due to normal physiological changes in the body like decreased arterial compliance, and are also more exposed to risk factors.

Restraints for the Heart Attack Diagnostics Market

Limited Access to Healthcare in Remote Areas

Inadequate healthcare infrastructure in rural or underdeveloped regions significantly hinders the early diagnosis and treatment of heart attacks, exacerbating health disparities. These areas often lack essential medical facilities, diagnostic equipment, and trained healthcare professionals, making it challenging to identify and manage cardiovascular emergencies promptly. Limited access to advanced diagnostic tools such as ECG machines, blood tests for cardiac biomarkers, and imaging technologies further delays critical interventions. Additionally, the scarcity of specialized cardiac care centers means patients must travel long distances, which can be life-threatening in acute situations. Poor road connectivity and transportation options in these regions add to the challenges, often leading to preventable deaths.

Opportunity in the Heart Attack Diagnostics Market

Personalized Medicine and Biomarkers

The growth of precision medicine is revolutionizing heart attack diagnostics by fostering the use of biomarkers for targeted and personalized approaches. Biomarkers, such as troponins, creatine kinase-MB, and natriuretic peptides, provide critical insights into the physiological and biochemical changes associated with heart attacks, enabling early and accurate detection. Precision medicine leverages these biomarkers to identify individual risk profiles, predict disease progression, and tailor diagnostic and treatment strategies to specific patient needs. This approach not only improves diagnostic accuracy but also minimizes unnecessary interventions and associated healthcare costs.

Advances in genomics and proteomics further enhance biomarker discovery, enabling the development of highly specific tests that can differentiate between various types of cardiovascular events. The integration of these biomarkers with advanced technologies, such as AI and big data analytics, allows for real-time monitoring and predictive modeling, paving the way for more effective and patient-centric care in heart attack diagnostics.

Trends for the Heart Attack Diagnostics Market

Shift Towards Non-Invasive Diagnostics

The rising demand for safer, non-invasive diagnostic methods, such as blood-based biomarkers, is transforming the landscape of heart attack diagnostics. Traditional diagnostic techniques, including invasive procedures like angiography, can be uncomfortable, costly, and carry risks of complications. In contrast, blood-based biomarker tests offer a simple, efficient, and minimally invasive alternative. These tests detect specific proteins, enzymes, or molecules released into the bloodstream during a heart attack, such as troponin, myoglobin, and creatine kinase-MB, providing critical information about cardiac health.

Non-invasive methods are especially appealing in emergency settings, where rapid, accurate diagnosis is essential for timely intervention. They are also preferred for regular monitoring of high-risk patients, reducing the need for repeated invasive procedures. Technological advancements have further enhanced the sensitivity and specificity of blood-based tests, enabling early detection and differentiation of cardiac events.

Segments Covered in the Report

By Test

o Computerized Cardiac Tomography

o Electrocardiogram

o Angiogram

o Blood Tests

o Other Tests

By End-User Vertical

o Hospitals

o Diagnostic Centers

o Ambulatory Surgical Centers

o Other End-User Verticals

Segment Analysis

By Test Analysis

On the basis of test, the market is divided into computerized cardiac tomography, electrocardiogram, angiogram, blood tests, and other tests. Among these, blood tests segment acquired the significant share in the market owing to their critical role in rapid and accurate diagnosis. Blood tests, such as those measuring cardiac biomarkers like troponin, creatine kinase-MB (CK-MB), and myoglobin, are widely regarded as the gold standard for detecting myocardial injury. These tests are minimally invasive, cost-effective, and provide quick results, making them indispensable in emergency settings where timely intervention is crucial.

By End-User Vertical Analysis

On the basis of end-user vertical, the market is divided into hospitals, diagnostic centers, ambulatory surgical centers, and other end-user verticals. Among these, hospitals segment held the prominent share of the market due to their comprehensive infrastructure, skilled medical professionals, and availability of advanced diagnostic tools. Hospitals are often the first point of care for heart attack patients, especially in emergency situations where immediate diagnosis and intervention are critical. The ability of hospitals to offer a wide range of diagnostic tests, including blood tests, electrocardiograms (ECGs), and imaging modalities like CT scans and angiograms, makes them the preferred choice for both patients and physicians.

Regional Analysis

North America Dominated the Market with the Highest Revenue Share

North America held the most of the share of 32.5% of the market driven by a combination of advanced healthcare infrastructure, a high prevalence of cardiovascular diseases, and significant investments in medical technology. The region boasts well-established healthcare systems that facilitate the widespread adoption of cutting-edge diagnostic tools, including advanced imaging systems, point-of-care testing devices, and AI-driven solutions. The rising incidence of heart attacks due to lifestyle factors, such as high obesity rates, sedentary habits, and poor dietary choices, has further fueled the demand for efficient diagnostic solutions.

Additionally, robust funding for research and development in the medical field has accelerated innovation, leading to the development of highly sensitive and accurate diagnostic methods. Favorable reimbursement policies and the presence of key market players like Abbott Laboratories, Roche Diagnostics, and Siemens Healthineers have also contributed to the region's dominance.

Competitive Analysis

The competitive analysis of the heart attack diagnostics market reveals a dynamic and rapidly evolving landscape, characterized by the presence of both established players and emerging companies innovating in diagnostic technologies. Major global players such as Abbott Laboratories, Roche Diagnostics, Siemens Healthineers, and GE Healthcare dominate the market due to their broad product portfolios, extensive distribution networks, and robust research and development capabilities. These companies offer a wide range of diagnostic tools, including blood-based tests, electrocardiograms, angiography equipment, and advanced imaging technologies, providing comprehensive solutions for heart attack detection.

Recent Developments

In June 2024, Philips has announced the launch of its Philips Cardiac Workstation, designed to revolutionize diagnostic cardiology. This new platform aims to improve patient care in cardiology and accelerate clinical decision-making across the Middle East, Africa (MEA), and Europe.

In April 2024, GE Healthcare introduced Caption AI on the Vscan Air SL, aiming to broaden access to cardiac care. This innovative technology enables more clinicians and medical professionals to capture diagnostic-quality cardiac images, enhancing the ability to provide effective cardiac assessments.

Key Market Players in the Heart Attack Diagnostics Market

o Hitachi Corporation

o GE Healthcare

o Koninklijke Philips NV

o F Hoffmann-La Roche Ltd

o Midmark Corporation

o Schiller AG

o Astrazenca PLC

o Toshiba Corporation

o Siemens Healthineers

o Welch Allyn Inc

o Other Key Players

|

Report Features |

Description |

|

Market Size 2023 |

USD 10.5 Billion |

|

Market Size 2033 |

USD 21.6 Billion |

|

Compound Annual Growth Rate (CAGR) |

7.4% (2023-2033) |

|

Base Year |

2023 |

|

Market Forecast Period |

2024-2033 |

|

Historical Data |

2019-2022 |

|

Market Forecast Units |

Value (USD Billion) |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

By Test, End-User Vertical, and Region |

|

Geographies Covered |

North America, Europe, Asia Pacific, and the Rest of the World |

|

Countries Covered |

The U.S., Canada, Germany, France, U.K, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil |

|

Key Companies Profiled |

Hitachi Corporation, GE Healthcare, Koninklijke Philips NV, F Hoffmann-La Roche Ltd, Midmark Corporation, Schiller AG, Astrazenca PLC, Toshiba Corporation, Siemens Healthineers, Welch Allyn Inc, and Other Key Players. |

|

Key Market Opportunities |

Personalized Medicine and Biomarkers |

|

Key Market Dynamics |

Rising Prevalence of Cardiovascular Diseases |

Frequently Asked Questions

1. Who are the key players in the Heart Attack Diagnostics Market?

Answer: Hitachi Corporation, GE Healthcare, Koninklijke Philips NV, F Hoffmann-La Roche Ltd, Midmark Corporation, Schiller AG, Astrazenca PLC, Toshiba Corporation, Siemens Healthineers, Welch Allyn Inc, and Other Key Players.

2. How much is the Heart Attack Diagnostics Market in 2023?

Answer: The Heart Attack Diagnostics Market size was valued at USD 10.5 Billion in 2023.

3. What would be the forecast period in the Heart Attack Diagnostics Market?

Answer: The forecast period in the Heart Attack Diagnostics Market report is 2024-2033.

4. What is the growth rate of the Heart Attack Diagnostics Market?

Answer: Heart Attack Diagnostics Market is growing at a CAGR of 7.4% during the forecast period, from 2024 to 2033.

Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

- Accurate & Verified Data:Our insights are trusted by global brands and Fortune 500 companies.

- Complete Transparency:No hidden fees, locked content, or misleading claims - ever.

- 24/7 Analyst Support:Our expert team is always available to help you make smarter decisions.

- Instant Savings:Enjoy a flat $1000 OFF on every report.

- Fast & Reliable Delivery:Get your report delivered within 5 working days, guaranteed.

- Tailored Insights:Customized research that fits your industry and specific goals.

Need custom data?

Get tailored segments, regions, competitors, or analyst support for this report.