Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

At Infinity Market Research, we do not just deliver data - we deliver clarity, confidence, and competitive edge.

In a world driven by insights, we help businesses unlock the infinite potential of informed decisions.

Here is why global brands, startups, and decision-makers choose us:

Industry-Centric Expertise

With deep domain knowledge across sectors - from healthcare and technology to manufacturing and consumer goods - our team delivers insights that matter.

Custom Research, Not Cookie-Cutter Reports

Every business is unique, and so are its challenges. Thats why we tailor our research to your specific goals, offering solutions that are actionable, relevant, and reliable.

Data You Can Trust

Our research methodology is rigorous, transparent, and validated at every step. We believe in delivering not just numbers, but numbers that drive real impact.

Client-Centric Approach

Your success is our priority. From first contact to final delivery, our team is responsive, collaborative, and committed to your goals - because you are more than a client; you are a partner.

Recent Reports

Obesity Management Market

GLP-1 Receptor Agonist Market

Residential Dry Construction Market

Residential Dry Construction Market Global Industry Analysis and Forecast (2024-2032) By Material Type(Plasterboard (Gypsum Board, Fiber Cement Board),Wood Panels, Metal Panels, Glass Panels, Plastic Panels),By System Type(Ceilings & Roofing Systems, Wall Systems, Flooring Systems, Partition Systems),By Construction Type(New Construction, Renovation & Remodeling),By Application(Single-Family Homes, Multi-Family Residential Buildings, Luxury Villas & High-End Residences) and Region

Mar 2025

Building and Construction

Pages: 138

ID: IMR1871

Residential Dry Construction Market Synopsis

Residential Dry Construction Market research report acquired the significant revenue of XX Billion in 2023 and expected to be worth around USD XX Billion by 2032 with the CAGR of XX% during the forecast period of 2024 to 2032.

Growing demand for environmentally friendly, reasonably priced, and time-efficient building solutions is driving notable expansion in the Residential Dry Construction Market. Dry building reduces the usage of water and cement by depending on prefabricated materials, including gypsum board, fiber cement panels, and metal frames, unlike conventional wet building techniques. Key elements driving the acceptance of dry building in the residential sector are rising urbanization, a growing middle-class population, and changing inclination for lightweight and energy-efficient homes.

Technological developments in prefabrication and modular construction enable faster and more effective residential building methods, thereby transforming the market. Green building projects and the usage of environmentally friendly materials that reduce carbon footprints are under encouragement by governments all around. Fire-resistant, moisture-proof, and sound-insulating dry building materials are becoming increasingly popular among homeowners, further driving market expansion. Moreover, driving market demand is the growing attention paid to rehabilitation and remodeling initiatives in developed nations.

The market suffers difficulties like high beginning costs and lack of qualified workers for specialized dry building techniques even with its potential for expansion. Moreover, regional differences in building norms and rules can impede the growth of the market. Still, residential builders and developers are becoming more and more interested in dry construction's long-term benefits, such as lower maintenance costs, better durability, and faster project completion. This is especially true when you consider that strict energy efficiency standards and strong infrastructure investments are making North America and Europe the leading markets. Asia-Pacific is becoming a high-growth area due to rapid urbanization and housing sector expansion.

Residential Dry Construction Market Outlook, 2023 and 2032: Future Outlook

Residential Dry Construction Market Trend Analysis

Trend: Growing Adoption of Prefabrication and Modular Construction in Residential Projects

Rising acceptance of prefabrication and modular building techniques is driving notable expansion in the residential dry construction industry. Developers are turning to dry construction methods, which require less water and faster assembly, in response to growing demand for quicker, more affordable, and ecological housing alternatives. The increasing emphasis on energy efficiency and waste reduction has further fueled this trend, as dry construction methods offer superior insulation, reduced material waste, and improved structural performance. In order to solve the worldwide housing problem, governments and regulatory authorities are also encouraging this change by means of incentives and regulations favoring modular and prefabricated building.

Drivers: Rising Urbanization, Sustainable Building Practices, and Faster Construction Demand

Rising urbanization, the increasing acceptance of sustainable building techniques, and the demand for quicker construction methods are driving notable expansion of the Residential Dry Construction Market. Particularly in developing areas, rapid urban growth is driving demand for reasonably priced and effective housing options. Because they cut building time and labor costs, prefabricated components, including drywall, gypsum boards, and lightweight steel constructions—which comprise dry construction techniques—are becoming increasingly popular. These techniques help reduce waste output, in line with rules supporting environmentally friendly building materials and world sustainability objectives.

Restraints: High Initial Costs and Limited Awareness in Developing Regions

The substantial initial expenses connected with modern dry construction methods cause major limits on the residential dry construction market. Dry building materials, such as gypsum boards, fiber cement boards, and prefabricated panels, sometimes demand more upfront costs than conventional wet building techniques. Further adding to the financial load are the expenses of specialized equipment, trained workers, and premium raw materials. Furthermore, dry construction depends on exact engineering and installation, which might not always be possible for homes under budget control. These elements can deter adoption, especially in markets sensitive to prices where affordability is still a primary issue.

Opportunities: Advancements in Lightweight, Eco-friendly Materials and Increasing Renovation Activities

Thanks in large part to developments in lightweight and environmentally friendly materials, the market for residential dry building is expanding rapidly. While lowering environmental impact, innovations in gypsum board, fiber cement, and engineered wood panels are improving building efficiency. These materials improve indoor climate management, therefore contributing to energy-efficient dwellings even if they provide outstanding thermal and acoustic insulation. Also, stricter environmental laws and certifications for sustainable buildings are pushing manufacturers to make low-carbon-footprint alternatives, like bio-based composites and recycled drywall. This gives market players a lot of opportunities.

Residential Dry Construction Market Segment Analysis

Residential Dry Construction Market Segmented on the basis of By Material Type, By System Type, By Construction Type and By Application.

By Material

o Plasterboard (Gypsum Board, Fiber Cement Board)

o Wood Panels

o Metal Panels

o Glass Panels

o Plastic Panels

By Application

o Ceilings & Roofing Systems

o Wall Systems

o Flooring Systems

o Partition Systems

By Construction

o New Construction,

o Renovation & Remodelling

By Region

o North America (U.S., Canada, Mexico)

o Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe)

o Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe)

o Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC)

o Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa)

o South America (Brazil, Argentina, Rest of SA)

By Material Type, Plasterboard (Gypsum Board, Fiber Cement Board) segment is expected to dominate the market during the forecast period

Driven by growing acceptance of lightweight, ecological, and reasonably priced building materials, the market for residential dry construction is seeing constant expansion. Among these, plasterboard (containing gypsum board and fiber cement board) rules because of its cost, simplicity of installation, and fire-resistant qualities. Wood panels, which offer insulation advantages and visual attractiveness, often form interior walls and ceilings. Typically used for exterior cladding, metal panels offer structural strength and longevity. While plastic panels are a lightweight, moisture-resistant choice for many uses, glass panels are becoming more and more popular for modern architectural designs since they guarantee natural light penetration and energy efficiency.

The growing need for environmentally friendly and energy-efficient homes is driving even more innovation in dry construction materials. Leveraging these materials for faster assembly and lower labor costs, builders and homeowners are choosing prefabricated and modular building techniques more and more. Especially in developed countries, strict rules on sustainability and carbon footprint reduction are motivating the use of recyclable and renewable materials. Experts predict significant growth in the residential dry building industry in the coming years, as urbanization surges and smart housing solutions gain prominence.

By Application, Single-Family Homes segment expected to held the largest share

The Residential Dry Construction Market is experiencing significant growth, driven by the increasing demand for efficient, lightweight, and sustainable construction solutions. By application, the market is segmented into single-family homes, multi-family residential buildings, and luxury villas & high-end residences. Single-family homes dominate the segment due to the rising preference for independent living spaces and energy-efficient housing. Meanwhile, multi-family residential buildings are gaining traction in urban areas, fueled by rapid urbanization and the need for cost-effective housing solutions. Luxury villas and high-end residences also contribute to market growth, with premium materials and advanced dry construction techniques enhancing aesthetics and durability.

Innovations in prefabricated systems, drywall technology, and eco-friendly materials are propelling the adoption of dry construction across these segments. The method offers several advantages, such as reduced construction time, improved thermal and acoustic insulation, and lower labor costs. Additionally, sustainability concerns and stringent building regulations are encouraging developers to shift toward dry construction techniques. With increasing investments in housing infrastructure and a growing focus on green building practices, the residential dry construction market is set for steady expansion across diverse residential applications.

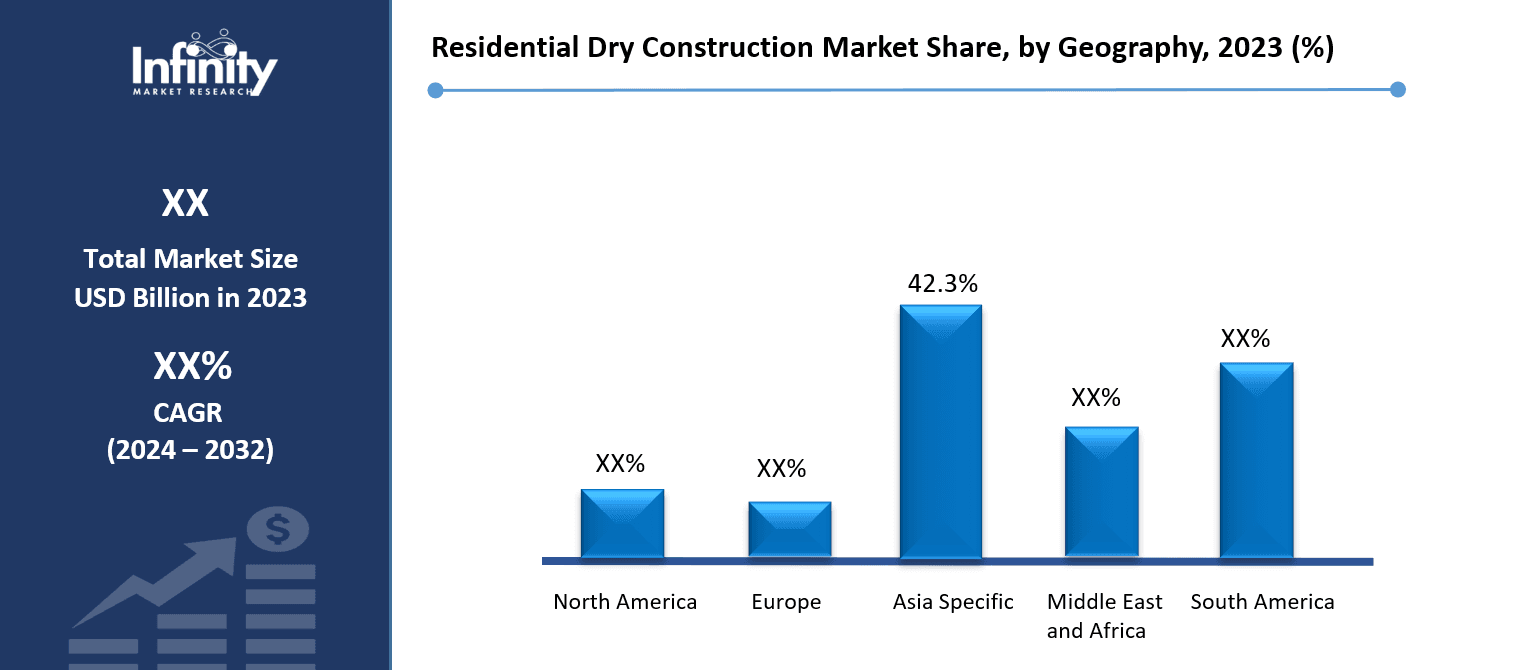

Residential Dry Construction Market Regional Insights:

Asia Pacific is Expected to Dominate the Market Over the Forecast period

Rising disposable incomes, rapid urbanization, and a growing population are likely to drive the Asia-Pacific region to dominate the residential dry construction market throughout the forecast period. Driven by government projects supporting inexpensive housing and sustainable building techniques, nations including China, India, and Japan are seeing an increase in residential construction activity. There is also a strong focus in the region on using environmentally friendly and energy-efficient building techniques. This is leading to a rise in demand for dry building techniques, which offer benefits such as shorter construction times, less material waste, and longer-lasting structures.In the Asia-Pacific region, the market is also growing because building technologies are getting better and lighter materials like gypsum boards, plasterboards, and fiber cement panels are becoming more popular. Growing knowledge of environmental issues and strict rules encouraging sustainable building are also driving market expansion. Furthermore, the growing trend of prefabricated and modular homes in metropolitan regions increases demand for dry building solutions, so Asia-Pacific leads the market in this field.

Residential Dry Construction Market Share, by Geography, 2023 (%)

Active Key Players in the Residential Dry Construction Market

o Saint-Gobain S.A. (France)

o Knauf Gips KG (Germany)

o Etex Group (Belgium)

o USG Corporation (United States)

o LafargeHolcim Ltd. (Switzerland)

o Armstrong World Industries, Inc. (United States)

o Georgia-Pacific LLC (United States)

o Gyproc India (a subsidiary of Saint-Gobain) (India)

o Fletcher Building Limited (New Zealand)

o CSR Limited (Australia)

o Others

Global Residential Dry Construction Market Scope

|

Global Residential Dry Construction Market | |||

|

Base Year: |

2023 |

Forecast Period: |

2024-2032 |

|

Historical Data: |

2017 to 2023 |

Market Size in 2023: |

USD XXX Billion |

|

Forecast Period 2024-32 CAGR: |

XXX% |

Market Size in 2032: |

USD XXX Billion |

|

Segments Covered: |

By Material Type |

· Plasterboard (Gypsum Board, Fiber Cement Board) · Wood Panels · Metal Panels · Glass Panels · Plastic Panels | |

|

By System Type |

· Ceilings & Roofing Systems · Wall Systems · Flooring Systems · Partition Systems | ||

|

By Construction Type |

· New Construction, · Renovation & Remodelling | ||

|

By Application |

· Single-Family Homes, · Multi-Family Residential Buildings · Luxury Villas & High-End Residences | ||

|

By Region |

· North America (U.S., Canada, Mexico) · Eastern Europe (Bulgaria, The Czech Republic, Hungary, Poland, Romania, Rest of Eastern Europe) · Western Europe (Germany, UK, France, Netherlands, Italy, Russia, Spain, Rest of Western Europe) · Asia Pacific (China, India, Japan, South Korea, Malaysia, Thailand, Vietnam, The Philippines, Australia, New-Zealand, Rest of APAC) · Middle East & Africa (Turkey, Bahrain, Kuwait, Saudi Arabia, Qatar, UAE, Israel, South Africa) · South America (Brazil, Argentina, Rest of SA) | ||

|

Key Market Drivers: |

· Rising Urbanization, Sustainable Building Practices, and Faster Construction Demand | ||

|

Key Market Restraints: |

· High Initial Costs and Limited Awareness in Developing Regions | ||

|

Key Opportunities: |

· Advancements in Lightweight, Eco-friendly Materials and Increasing Renovation Activities | ||

|

Companies Covered in the report: |

· Saint-Gobain S.A. (France), Knauf Gips KG (Germany), Etex Group (Belgium), USG Corporation (United States), LafargeHolcim Ltd. (Switzerland), Armstrong World Industries, Inc. (United States), Georgia-Pacific LLC (United States), Gyproc India (a subsidiary of Saint-Gobain) (India), Fletcher Building Limited (New Zealand), CSR Limited (Australia), Others. | ||

Frequently Asked Questions

1. What would be the forecast period in the Residential Dry Construction Market research report?

Answer: The forecast period in the Residential Dry Construction Market research report is 2024-2032.

2. Who are the key players in the Residential Dry Construction Market?

Answer: Saint-Gobain S.A. (France), Knauf Gips KG (Germany), Etex Group (Belgium), USG Corporation (United States), LafargeHolcim Ltd. (Switzerland), Armstrong World Industries, Inc. (United States), Georgia-Pacific LLC (United States), Gyproc India (a subsidiary of Saint-Gobain) (India), Fletcher Building Limited (New Zealand), CSR Limited (Australia), Others.

3. What are the segments of the Residential Dry Construction Market?

Answer: The Residential Dry Construction Market is segmented into By Material Type, By System Type, By Construction Type, By Application, and region. By Material Type(Plasterboard (Gypsum Board, Fiber Cement Board),Wood Panels, Metal Panels, Glass Panels, Plastic Panels),By System Type(Ceilings & Roofing Systems, Wall Systems, Flooring Systems, Partition Systems),By Construction Type(New Construction, Renovation & Remodeling),By Application(Single-Family Homes, Multi-Family Residential Buildings, Luxury Villas & High-End Residences). By region, it is analyzed across North America (U.S.; Canada; Mexico), Eastern Europe (Bulgaria; The Czech Republic; Hungary; Poland; Romania; Rest of Eastern Europe), Western Europe (Germany; UK; France; Netherlands; Italy; Russia; Spain; Rest of Western Europe), Asia-Pacific (China; India; Japan; Southeast Asia, etc.), South America (Brazil; Argentina, etc.), Middle East & Africa (Saudi Arabia; South Africa, etc.).

4. What is the Residential Dry Construction Market?

Answer: Residential Dry Construction refers to a building technique that utilizes prefabricated and lightweight materials such as gypsum boards, fiber cement panels, metal frames, and composite materials to construct walls, ceilings, floors, and partitions without the use of water-based materials like concrete or mortar. This method is widely adopted in modern housing projects due to its efficiency, sustainability, and cost-effectiveness, allowing for faster construction, reduced labor costs, and minimal environmental impact. It is particularly favored for energy-efficient homes, modular housing, and renovation projects, offering benefits such as enhanced thermal insulation, soundproofing, and improved fire resistance compared to traditional wet construction techniques.

Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

- Accurate & Verified Data:Our insights are trusted by global brands and Fortune 500 companies.

- Complete Transparency:No hidden fees, locked content, or misleading claims - ever.

- 24/7 Analyst Support:Our expert team is always available to help you make smarter decisions.

- Instant Savings:Enjoy a flat $1000 OFF on every report.

- Fast & Reliable Delivery:Get your report delivered within 5 working days, guaranteed.

- Tailored Insights:Customized research that fits your industry and specific goals.

Need custom data?

Get tailored segments, regions, competitors, or analyst support for this report.