Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

At Infinity Market Research, we do not just deliver data - we deliver clarity, confidence, and competitive edge.

In a world driven by insights, we help businesses unlock the infinite potential of informed decisions.

Here is why global brands, startups, and decision-makers choose us:

Industry-Centric Expertise

With deep domain knowledge across sectors - from healthcare and technology to manufacturing and consumer goods - our team delivers insights that matter.

Custom Research, Not Cookie-Cutter Reports

Every business is unique, and so are its challenges. Thats why we tailor our research to your specific goals, offering solutions that are actionable, relevant, and reliable.

Data You Can Trust

Our research methodology is rigorous, transparent, and validated at every step. We believe in delivering not just numbers, but numbers that drive real impact.

Client-Centric Approach

Your success is our priority. From first contact to final delivery, our team is responsive, collaborative, and committed to your goals - because you are more than a client; you are a partner.

Recent Reports

Obesity Management Market

GLP-1 Receptor Agonist Market

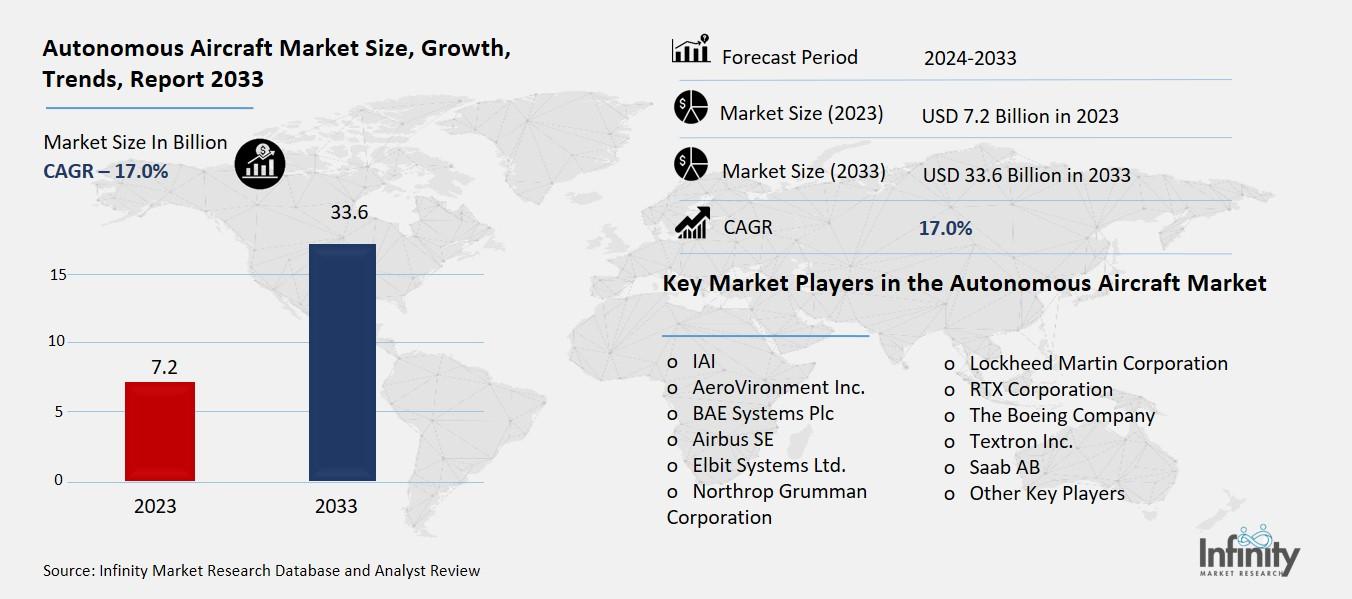

Autonomous Aircraft Market

Global Autonomous Aircraft Market (By Technology, Fully Autonomous and Increasingly Autonomous (IA); By Component, Propulsion Systems, Radars & Transponders, Actuation System, Flight Management Computers, Air Data Inertial Reference Units, and Other Components; By End-User, Defense, Air Medical Service, Cargo & Delivery Aircraft, Commercial Aircraft, and Other End-Users, By Region and Companies), 2024-2033

Jan 2025

Aerospace and Defense

Pages: 138

ID: IMR1397

Autonomous Aircraft Market Overview

Global Autonomous Aircraft Market acquired the significant revenue of 7.1 Billion in 2023 and expected to be worth around USD 33.6 Billion by 2033 with the CAGR of 17.0% during the forecast period of 2024 to 2033. The market of autonomous aircraft around the world is growing no small amount owing to the improvement of AI, sensors, and improved demand for better and more cost-efficient and safer aviation. Such unmanned aircraft which can fly themselves are increasingly being deployed in different domains such as civil and business aviation, armed forces use, delivery and distribution and urban air transport systems. Some of the main drivers encouraging market growth are a growing appreciation of UAVs for surveillance and delivery as well as passenger and investment by aerospace giants in autonomous flight solutions.

Drivers for the Autonomous Aircraft Market

Advancements in AI and Automation Technologies

Incorporation of artificial intelligence (AI) in the control and management of self-flying airplanes is transforming decision making by providing instant data analysis from various hardware such as sensors, cameras, and radar. These aircraft can also select their flight routes and altitudes, avoid other traffic, and control their environment and respond to distress calls autonomously using such algorithms. This makes it easier to implement operations and reduce on the likelihood of an occurrence of an accident particularly in congested airspace or during storm.

Furthermore, technology improvement in navigation and control system like high precision GPS, INS, and machine vision, enhance the precise flight trajectory control and raise the performance. Combined they support fully automated planes to function nearly independently and without much interference from human interferences reducing errors as well as improving efficiency through fuel conservation and time.

Restraints for the Autonomous Aircraft Market

High Initial Investment

The development of autonomous aircraft involves substantial costs in research and development (R&D), prototyping, and infrastructure upgrades, which pose significant barriers to entry. Designing and testing sophisticated AI-driven systems, advanced sensors, and robust cybersecurity measures require extensive investment, often making it challenging for smaller players to compete. Furthermore, the need for specialized infrastructure, such as autonomous flight control centers and maintenance facilities, adds to the financial burden. As a result, small and medium enterprises (SMEs) face limited adoption of autonomous aircraft due to their constrained budgets and resources, often leaving the market dominated by large, well-funded aerospace and technology companies. This financial disparity slows the democratization of the technology and its widespread deployment across diverse industries.

Opportunity in the Autonomous Aircraft Market

Emerging Applications in Logistics and Delivery

The growing adoption of autonomous drones is revolutionizing delivery services, particularly in e-commerce and healthcare. Companies like Amazon, Zipline, and DHL are utilizing drones to enhance last-mile delivery, offering faster and more efficient services, especially in urban and suburban areas. In healthcare, drones are being deployed to transport time-sensitive medical supplies, such as blood, vaccines, and emergency medications, directly to hospitals or clinics. This approach not only reduces delivery times but also ensures critical supplies reach areas where traditional logistics face delays, making drones an essential tool for modern supply chains.

Autonomous drones are increasingly being used to serve remote and hard-to-reach locations, overcoming barriers such as mountainous terrain, dense forests, or islands. These regions, often underserved by conventional transportation networks, benefit from drone technology for delivering essential goods, conducting infrastructure inspections, and supporting disaster relief operations. For instance, drones are being used to deliver emergency aid and medical supplies to disaster-stricken areas where roads and bridges are inaccessible. This capability is transforming logistics in remote regions, making critical services faster, more reliable, and more cost-effective.

Trends for the Autonomous Aircraft Market

Increased Investments in AI-Driven Flight Systems

Machine learning (ML) is playing a pivotal role in enhancing the reliability and efficiency of autonomous aircraft. By analyzing vast datasets collected from onboard sensors, ML algorithms can predict potential maintenance issues before they lead to failures, minimizing downtime and reducing operational costs. Additionally, these algorithms enable real-time adjustments by continuously monitoring variables such as weather conditions, flight dynamics, and system performance. This adaptability ensures optimal performance and safety during flight, even in rapidly changing environments.

Autonomous aircraft equipped with advanced AI and ML systems can make informed decisions even in challenging scenarios, such as extreme weather, unexpected obstacles, or system malfunctions. These systems process and analyze real-time data to devise optimal solutions, ensuring the aircraft maintains stability and safety. For instance, during severe turbulence or equipment failure, the aircraft can autonomously adjust its route, altitude, or speed to mitigate risks. This level of decision-making not only reduces dependence on human intervention but also enhances the resilience and reliability of autonomous operations.

Segments Covered in the Report

By Technology

o Fully Autonomous

o Increasingly Autonomous (IA)

By Component

o Propulsion Systems

o Radars & Transponders

o Actuation System

o Flight Management Computers

o Air Data Inertial Reference Units

o Other Components

By End-User

o Defense

o Air Medical Service

o Cargo & Delivery Aircraft

o Commercial Aircraft

o Other End-Users

Segment Analysis

By Technology Analysis

On the basis of technology, the market is divided into fully autonomous and increasingly autonomous (IA). Among these, increasingly autonomous (IA) segment acquired the significant share in the market owing to its gradual and adaptive integration into existing aviation ecosystems. IA systems combine automated functionalities with human oversight, offering a balance between autonomy and control, which appeals to regulators and operators concerned about safety and reliability. These systems are particularly favored in commercial and military applications, where incremental automation improves operational efficiency while maintaining a layer of human intervention for critical decision-making.

The IA segment benefits from faster adoption as it aligns with current regulatory frameworks and addresses concerns regarding fully autonomous systems, making it a more practical and widely accepted option in the transitional phase toward full autonomy.

By Component Analysis

On the basis of component, the market is divided into propulsion systems, radars & transponders, actuation system, flight management computers, air data inertial reference units, and other components. Among these, flight management computers segment held the prominent share of the market due to their critical role in ensuring safe and efficient flight operations. Flight management computers are responsible for processing complex flight data, managing flight plans, and optimizing route navigation. They integrate inputs from various systems, including propulsion, sensors, and environmental data, enabling real-time decision-making and adjustments during flight. Their ability to automate key functions such as altitude control, speed regulation, and route planning enhances operational efficiency and reduces human error.

By End-User Analysis

On the basis of end-user, the market is divided into defense, air medical service, cargo & delivery aircraft, commercial aircraft, and other end-users. Among these, defense segment held the prominent share of the market due to the increasing demand for unmanned aerial vehicles (UAVs) and autonomous aircraft in military applications. These aircraft are primarily used for surveillance, reconnaissance, intelligence gathering, and precision strikes, offering significant advantages in terms of reduced risk to human life and operational efficiency. The defense sector’s need for high-performance, stealthy, and cost-effective solutions further drives the adoption of autonomous systems. Additionally, the growing focus on advanced technologies such as AI, machine learning, and automation in defense strategies strengthens the reliance on autonomous aircraft for mission-critical operations, boosting the market share of this segment.

Regional Analysis

North America Dominated the Market with the Highest Revenue Share

North America held the most of the share of 34.2% of the market. The region is home to leading aerospace and defense companies such as Boeing, Lockheed Martin, and Northrop Grumman, which are at the forefront of developing and deploying autonomous aircraft technologies. Strong investments in research and development, along with a robust technological infrastructure, contribute to North America's leadership in this market.

Additionally, the U.S. government’s significant funding for defense applications and the increasing demand for unmanned aerial vehicles (UAVs) in military, commercial, and cargo sectors further support market growth. The region also benefits from favorable regulatory frameworks, which enable faster integration of autonomous aircraft into commercial and defense operations. With a high level of innovation, strong defense budgets, and a growing demand for autonomous solutions, North America is expected to maintain its dominant position in the market.

Competitive Analysis

The competitive analysis of the autonomous aircraft market reveals a highly dynamic and rapidly evolving landscape, characterized by the presence of both established aerospace giants and emerging startups. Major players, such as Boeing, Lockheed Martin, Northrop Grumman, and Airbus, dominate the market, leveraging their vast resources, technical expertise, and strong industry relationships to develop cutting-edge autonomous technologies for both defense and commercial applications. These companies are focusing heavily on research and development to integrate artificial intelligence, machine learning, and advanced sensors into their autonomous aircraft solutions.

Recent Developments

In May 2024, Northrop Grumman, in partnership with DARPA, advanced its autonomous VTOL aircraft design during Phase 1b of the ANCILLARY program. The collaboration with Leigh Aerosystems and Near Earth Autonomy focused on improving modeling, testing subsystems, and reducing technical risks, aiming to develop an affordable solution for the warfighter community.

In October 2022, Joby Aviation Inc. acquired Xwing Inc.'s autonomy division to accelerate its U.S. Department of Defense contract deliverables and expand future contract opportunities. The acquisition includes all of Xwing's automation and autonomy technologies.

Key Market Players in the Autonomous Aircraft Market

o IAI

o AeroVironment Inc.

o Airbus SE

o Elbit Systems Ltd.

o Northrop Grumman Corporation

o Lockheed Martin Corporation

o RTX Corporation

o The Boeing Company

o Textron Inc.

o Saab AB

o Other Key Players

|

Report Features |

Description |

|

Market Size 2023 |

USD 7.1 Billion |

|

Market Size 2033 |

USD 33.6 Billion |

|

Compound Annual Growth Rate (CAGR) |

17.0% (2023-2033) |

|

Base Year |

2023 |

|

Market Forecast Period |

2024-2033 |

|

Historical Data |

2019-2022 |

|

Market Forecast Units |

Value (USD Billion) |

|

Report Coverage |

Revenue Forecast, Market Competitive Landscape, Growth Factors, and Trends |

|

Segments Covered |

By Technology, Component, End-User, and Region |

|

Geographies Covered |

North America, Europe, Asia Pacific, and the Rest of the World |

|

Countries Covered |

The U.S., Canada, Germany, France, U.K, Italy, Spain, China, Japan, India, Australia, South Korea, and Brazil |

|

Key Companies Profiled |

IAI, AeroVironment Inc., BAE Systems Plc, Airbus SE, Elbit Systems Ltd., Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, The Boeing Company, Textron Inc., Saab AB, and Other Key Players. |

|

Key Market Opportunities |

Emerging Applications in Logistics and Delivery |

|

Key Market Dynamics |

Advancements in AI and Automation Technologies |

Frequently Asked Questions

1. Who are the key players in the Autonomous Aircraft Market?

Answer: IAI, AeroVironment Inc., BAE Systems Plc, Airbus SE, Elbit Systems Ltd., Northrop Grumman Corporation, Lockheed Martin Corporation, RTX Corporation, The Boeing Company, Textron Inc., Saab AB, and Other Key Players.

2. How much is the Autonomous Aircraft Market in 2023?

Answer: The Autonomous Aircraft Market size was valued at USD 7.2 Billion in 2023.

3. What would be the forecast period in the Autonomous Aircraft Market?

Answer: The forecast period in the Autonomous Aircraft Market report is 2024-2033.

4. What is the growth rate of the Autonomous Aircraft Market?

Answer: Autonomous Aircraft Market is growing at a CAGR of 17.0% during the forecast period, from 2024 to 2033.

Secure Payment Guaranteed

Safe checkout with trusted global payment methods.

Why Choose Infinity Market Research?

- Accurate & Verified Data:Our insights are trusted by global brands and Fortune 500 companies.

- Complete Transparency:No hidden fees, locked content, or misleading claims - ever.

- 24/7 Analyst Support:Our expert team is always available to help you make smarter decisions.

- Instant Savings:Enjoy a flat $1000 OFF on every report.

- Fast & Reliable Delivery:Get your report delivered within 5 working days, guaranteed.

- Tailored Insights:Customized research that fits your industry and specific goals.

Need custom data?

Get tailored segments, regions, competitors, or analyst support for this report.